Travelport has completed the integration of corporate booking tool Deem, which it acquired earlier this year.

Travelport — along with its two larger competitors, public companies Amadeus and Sabre — primarily act as marketplaces to connect airlines and travel agents.

While Amadeus and Sabre have had in-house corporate travel booking tools in recent years, Travelport has not since it sold Locomote in 2019.

The Deem tool is now part of Travelport+, the next generation of the booking platform for travel agents that Travelport has been developing over the past two years. And agencies that had been using Deem can now access Travelport data through the platform, which is still also compatible with data from Amadeus and Sabre.

The software from Deem is meant to provide travel agents a simpler, more modern experience than has been historically available for corporate travel. And the software includes a tool that travelers can use to manage their own trips.

“It extends the vision that we set for Travelport back in 2019 or early 2020, which was we wanted to create a more modern retailing experience that was more akin to what leisure travelers might experience,” said John Elieson, chief operating officer and deputy CEO of Travelport.

“You go to a site like Travelocity or Expedia or Priceline, and you’ve just got this really intuitive, enjoyable experience. And yet in corporate travel, it’s just much clunkier.”

Travelport CEO Greg Webb said early this year that more than 80% of the company’s travel agent customers were using Travelport+ at that time, and the rest were expected to transition in the following 12 to 18 months.

Infare, a Denmark-based provider of airfare data and analysis software, has been acquired.

OAG, a UK-based provider of flight status and schedule information, said Friday that it has acquired Infare from private equity firm Ventiga Capital. The firm had owned Infare since 2017.

The price and terms of the latest deal were not disclosed.

OAG and Infare had been in a partnership that was announced in April 2022.

OAG said the deal values the combined company at over $500 million. The combined company has 300 employees in 10 offices.

OAG said that both management teams will continue with the company and retain a shareholding, with fresh backing from Vitruvian Partners. Vitruvian Partners bought OAG from Axio Group for $215 million in 2017.

“The increasing dynamism in global travel and technology is fueling a need for more sophisticated, granular data to understand, manage, and unlock growth in air travel,” said Phil Callow, CEO of OAG, in a statement. “The acquisition of Infare strengthens our ability to deliver consistent and accurate information across the wider supply and demand value chain.”

Expensya, the corporate expense management startup, has been acquired.

The Tunisia-based company said Tuesday that the deal is now complete with buyer Medius, the New York-based provider of accounts payable automation software.

Terms were not disclosed.

Medius’s software primarily deals with invoices, processing, and payments. The Expensya software automates the processing of employee expenses.

Medius said it completed the acquisition to give its clients a more complete set of services, and the deal also expands the buyer’s clients base into new regions.

Medius said it has more than 4,000 customers in 102 countries. Expensya has more than 6,000 clients in 100 countries, with a workforce of 200 employees.

“Expensya’s AI capabilities, employee spend management solution, and payment cards, with Medius’s AP automation platform, means we can now cover the whole indirect spend of companies and can apply the power of AI to help finance teams to optimize cost and processes across the board,” said Karim Jouini, CEO of Expensya, in a statement.

Expensya had raised a total of $25.6 million over four funding rounds, according to Crunchbase. The most recent raises were a $20 million series B round in 2021 and $4.5 million in 2018.

The story of Culture Trip is sordid, and in the scheme of things, an inconsequential blip on the face of heavily funded travel startups.

What was at some point was an SEO-fueled destination content factory that had raised a lot of money and failed to create enough revenues, it tried to pivot into being an online travel agency and failed at that, the company somehow pivoted into being a small-group tour company — a reseller of tours from the likes of Intrepid Travel and others — in the last year and no one noticed.

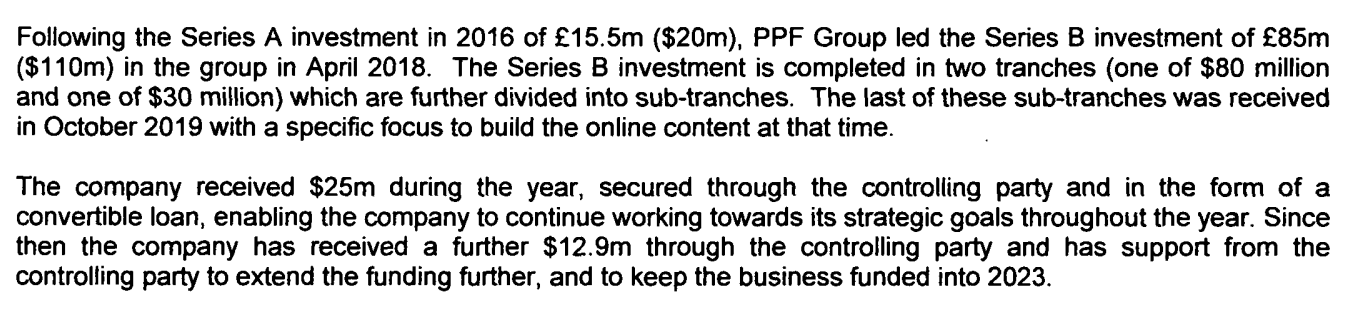

Now, after raising as much as $175 million in equity and debt (see the details from its UK Companies House filing, the screenshot posted above) over the 12 years of its existence, it announced Tuesday that the company did a management buyout led by CEO Ana Jakimovska recently and has also put up the company for sale, or investment. Clearly the majority investor PPF Group lost its shirt in this deal, that’s for sure.

“At the beginning of 2022, Culture Trip launched an exciting new strategy, selling unique curated trips to digital savvy millennials using their digital content to acquire customers. The business has undergone rapid growth since this pivot, achieving an impressive 30% quarter-on-quarter growth and 78% year-on-year growth,” the company touted in the release Tuesday.

OK, lets unpack that: According to the financial filings, it made a whopping $1.9 million in revenues in 2021 with losses of $23.5 million for the year. And if we take the company figures at face value, that its revenues increased by 78 percent in the last year, even being generous its revenues for 2022 were around $3 million (see screenshot below), even if, as the company claimed, its losses have narrowed.

The company, which according to our estimates has gotten rid of most of its employees during 2022 (it had about 130 or so in 2021), is now trying to sell itself. It also announced Tuesday that it has hired advisory firm Lazarus Consulting to start a sale process or get an investment.

With little to no brand value, any residual SEO value quickly deteriorating and little revenues to boast of, and likely being unprofitable as a business, it is hard to see any good outcomes from here.

Skift editors were struck by this chart of Wyndham’s stock price as of Friday. Investors continue to behave as if it would be a good thing for the world’s largest hotel franchisor to merge with another player. Sustained investor pressure on that score might prompt Wyndham’s management to change strategy at some point.

So why would investors cheer an offer for Wyndham?

Baird Equity Research held meetings with Wyndham’s management team after the announcement.

“The company continues to believe the stock is trading at a ‘significant and unwarranted discount,'” wrote the Baird analysts, who agree with management’s view.

To be clear, Baird analysts like Wyndham’s management and neither call for nor predict a merger. But in a flash report, Baird analysts suggested some reasons about why Wyndham’s stock had “underperformed” before the merger rumors.

“The list of potential reasons (among others) includes: growing competition in the lower-end chain scales; recent banking/financing uncertainties that might disproportionately impact Wyndham’s development pipeline; and Wyndham’s typical customer, which has an average household income of $91K, potentially being more impacted from a disposable income perspective due to continued inflationary pressures.”

—Michael Bellisario and Jo Choy of Baird.

Wyndham’s management had retorts to every concern. They said they saw no signs of fundamental slowing in leisure travel demand or in hotel development deal flow, signings, and ability to meet announced targets. Only about two dozen deals in its pipeline appear to face any risk of headwinds because of trouble getting financing because of recent banking and interest rate turmoil.

And yet, the market continues to value Wyndham more when they believe it’s in play. That partly reflect’s an investor mentality. Analyst David Katz at Jeffries estimated this week that any takeover bid might come with a price premium of as much as 30 percent of Wyndham’s stock prices. Some investors, possibly naive, are looking for a quick gain.

Yet Wyndham has weaker earnings growth forecasts for 2024 when compared with Choice Hotels, its competitor with the most overlap in hotel profile.

To paraphrase Baird’s Michael Bellisario and Jo Choy, risks to Wyndham include:

the sustainability of brand equity and customer loyalty when facing the larger loyalty and co-branded credit card machines of players like Marriott International

the endurance of its popularity among developers especially as larger groups like Hilton and Hyatt increasingly develop brands in the premium economy sector that Wyndham has heavy exposure to

exposure to a more price-conscious traveler during macroeconomic headwinds in the context of rivalry from other hotel brand companies

Wyndham’s management capably managed its way through the pandemic and have consistently met their announced targets while avoiding unpleasant surprises. Yet Wyndham’s trades at a noticeable discount to the sum of its parts, according to a few investment banks that cover the stock.

It appears that some investors believe Wyndham would be stronger as part of a larger group that could have more scale efficiencies, such as in a larger loyalty program, an ability to negotiate deeper discounts on things like furniture supplies and commissions for distribution, and back-office synergies.

If investors continue to signal with their pricing behavior frustration with Wyndham for a year or longer, pressure will only grow on Wyndham’s management to adjust their business strategy in response or possibly entertain merger talks.

Lufthansa finally has a deal. For ITA Airways that is, and according to reports.

The Frankfurt-based carrier will initially buy 40 percent of the state-owned Italian airline for $343-354 million (€320-330 million), according to a report by Italian daily Corriere Della Sera. Lufthansa would invest a further $537 million to raise its stake in ITA to up to 95 percent at a later date. A final agreement could be signed as soon as Thursday.

An ITA Airways Airbus A330-900. (ITA Airways)

The deal is the culmination of years of effort by Lufthansa to buy its way into the Italian market. The German carrier bid for a stake in ITA’s predecessor Alitalia as early as 2008, only to be out maneuvered by Air France-KLM. In the latest round of dealmaking, Lufthansa was counted out last year when a Certares-led consortium of Air France-KLM and Delta Air Lines was selected as the preferred bidder. But that deal fell through and Lufthansa was back in the running by December; the group made an official offer in January. Air France-KLM has, meanwhile, shifted its interest to acquiring TAP Air Portugal.

Lufthansa Group CEO Carsten Spohr has described the group as the “natural home” for ITA. Italy is Lufthansa’s largest market outside of its home markets, which include Austria (Austrian Airlines), Germany (Lufthansa and Eurowings), and Switzerland (Swiss Air). In May, Spohr said ITA’s Rome hub could be an integral southern gateway to Africa and Latin America for the group.

Lufthansa and the Italian government will need to European Union antitrust sign off before any deal for ITA could close.

Sunwing will continue to operate as independent airline for the foreseeable future, but could be integrated into WestJet or its budget subsidiary Swoop in the future. Sunwing Vacations is to become part of the WestJet’s Vacations Business.

“Investing further in leisure and sun flying across Canada is a critical driver for growth,” WestJet CEO Alexis von Hoensbroech said in a statement. “It brings me great pleasure to welcome Sunwing to the group … Together, we will strategically enhance our sun and leisure offerings to bring even more affordable and accessible travel opportunities to Canadians.”

Speaking on the airline’s new strategy with Airline Weekly in April, Von Hoensbroech said: “We have decided that we need to refocus WestJet on those things that made WestJet successful in the first place. And this is everything that is centered around Western Canada, this is everything centered around leisure flying for all of Canada, for East and West, and it’s around being a low-cost brand and low-cost airline.”

Sunwing boosts WestJet’s presence on routes to leisure destinations in the Caribbean and Mexico from Canada’s big eastern cities — Montreal, Ottawa, and Toronto — according to Diio by Cirium schedules. These are markets where WestJet has retrenched during the past year as part of its pivot towards more flying in Western Canada.

In the second quarter, WestJet and Swoop together, and Sunwing each have a 22 percent share of airline seats between Canada and the Caribbean and Mexico, Diio data show. Canada’s largest carrier, Air Canada, has a 24 percent share. The merger will give WestJet a 44 percent share of this lucrative market.

The value of WestJet’s acquisition of Sunwing was not disclosed.

Whether Viva Air will ever fly again is increasingly an open question. Avianca, which wants to merge with the bankrupt budget carrier, said late Wednesday that the conditions laid out by Colombian civil aviation regulators for the deal “make Viva’s recovery impossible.”

“Several conditions that, depending on the case, (i) make Viva’s operation unviable in the medium term, sentencing it to operational and financial failure (e.g. lack of slots), (ii) are impossible to comply with, given the current reality of that company, which has already lost more than half of its aircraft (e.g. the requirement to maintain capacity on exclusive routes despite the lack of aircraft and slots), or (iii) grant unjustified benefits to third parties (e.g. requiring Avianca to pay for Satena’s IOSA certification).”

— Avianca in its response to regulator Aerocivil’s tentative approval of the merger

The Bogotá-based Star Alliance carrier added that the conditions were “unfeasible” for the deal to move forward.

Aerocivil’s conditions include divesting slots at Bogotá’s congested El Dorado airport, reviving the Viva Air brand, honoring the tickets of travelers affected by Viva’s shutdown, and maintaining a codeshare with Colombian regional airline Satena.

Avianca first acquired Viva in mid-2022, and then announced plans to merge with the Colombian discounter — but maintain it as a separate brand — last August. What’s followed is a telenovela of twists and turns including allegations of antitrust violations by Avianca, 11th hour interferencefrom competitors, and mixed messages from Aerocivil.

What happens next is anyone’s guess. Viva closed its doors two months ago at the end of February and, as Avianca, points out, aircraft leasing companies have already begun taking back aircraft. Latam Airlines has begun offering former Viva staff jobs at its own growing Colombian subsidiary. And competitors, including Chilean discounter JetSmart and Copa Airlines-owned Wingo, have outlined plans to expand in the domestic Colombian market.

Aerocivil has said that Avianca, and other “interested parties” — including JetSmart, Latam, and Wingo — have 13 days to respond to its tentative approval. Only then, under the current timeline, could it finalize its approval and the deal close.

Yanolja Cloud has acquired Innsoft, an Oregon-based provider of hotel management software, for $8.3 million.

Yanolja Cloud is the hotel tech arm of South Korea-based booking platform Yanolja.

The acquisition is part of an effort to expand its hospitality services in North America, the company said Thursday.

Yanolja Cloud plans to leverage Innsoft’s resources to release a series of hospitality management solutions for the North American market as well as a new self check-in kiosk this year.

Innsoft offers various hotel management software solutions to booking platform companies including Booking.com and Expedia Group.

Yanolja Cloud said previously that it has big plans for hotel software sales, fueled by Softbank’s $1.7 billion investment in its parent company in 2021.

The company’s chief strategy officer last year said that it’s the company’s goal to overtake Oracle Hospitality as the global market leader in hotel operational software sales. At that time, the goal was that hoteliers would eventually be able to view Yanolja Cloud as a one-stop-shop for technology to run their operations, including bookings, distribution, and revenue management.

The potential merger of Avianca and Viva Air took a small step forward Wednesday when the former partially accepted the conditions laid out by the Colombian government for the combination of the country’s largest and third largest airlines.

While Avianca accepted regulator Aerocivil’s passenger protection provisions, including guaranteeing refunds for all travelers affected by Viva’s closure, it asked for “clarifications and minor modifications” to other conditions. The Star Alliance carrier asked that the remaining provisions, which include giving up slots at Bogotá’s congested El Dorado airport and committing to operating certain routes, reflect the “reality of the current market and to the operating conditions currently available to Viva.”

The latter point referred to Viva’s shutdown in February and subsequent repossession of several of its planes aircraft leasing companies. Then in March, budget competitor Ultra Air also shutdown, which upped pressure on the government to bring some budget airline capacity back to the Colombian domestic market, which had fully recovered to 2019 traveler numbers by October.

Avianca and Viva have called for “quick solutions” from Aerocivil in its response.

Latam, Avianca’s main competitor in South America, said Tuesday that it is seeking additional slots at the Bogotá airport from the merger. It added that, since Viva and Ultra shutdown, it has added five aircraft to its Colombian operation and increased the number of seats by 20 percent. Latam is backed by Delta Air Lines and Qatar Airways.

JetSmart, for its part, received a local operating certificate in March to begin domestic flights in Colombia. The Chilean discounter’s owners include U.S. private equity firm Indigo Partners and American Airlines.

The responses this week are the latest in what has turned into something of a soap opera over the future of the Colombian aviation market, which is the third largest in Latin America. Avianca, in the course of its takeover, may have violated local antitrust law after it took economic control of Viva last year and then, reportedly, installed a board to oversee the business that had its interests in mind. The airlines first sought approval to merge in August, a request that Aerocivil denied in November, and then reopened in January.

The Avianca-Viva merger is separate from Avianca’s plan to merge with Brazil’s Gol to create the new Abra Group.